Risk Neutral Pricing of Options II (Finance Course 3.2)

Risk Neutral Pricing of Options II (Finance Course 3.2)

(Advanced 🧠) How to price Options by way of Replication and Martingale probabilities.

Here are our quick notes on how to price an option through replication. I don’t know how much longer we are going to carry on doing these because, to be honest, I don’t think many of you care. lol

Risk Neutral Pricing

3 min read

Let’s now make a connection between replication and martingale pricing.

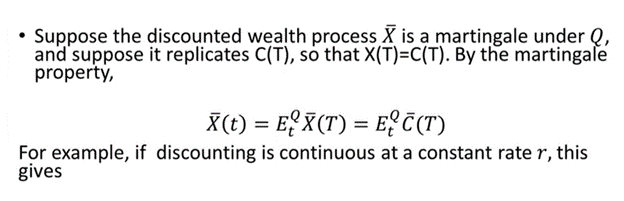

First, let’s show why it’s correct to price under martingale probabilities. Let’s assume that we have a wealth process X, which is under some probability Q. And suppose we can replicate a random payout C(T), so that X(T)=C(T). (Go back through our Finance Course series if you need a refresher.)

Look at the following.

If I look at the discounted value of wealth today X(t), by the martingale property (the first equality) which is equal to the expected value of the discounted future payoff under portfolio Q, we see that X(T), by replication, is actually equal to C(T).

So if we look at the formula below we see that the discounted cost of replicating is equal to the expected value of the discounted payoff of our option.

If we discount at rate r, and I move the discounting to the other side, this is the same as saying that X(t) is equal to condition expectation time t under q of the discounted future payoff C(T).

This (X(t)) is the cost of replicating C(T), and by definition, it has to be the price.

The cost of replication must be the price.

This is the main formula and it depends on two assumptions. One, there exists a martingale property, and the other is that I can replicate this claim.

The price of the option is the cost of replication therefore it’s equal to the expected value under Q of the discounted payoff.

It’s a very general formula for payoffs that can be replicated. It’s a formula that Black and Scholes didn’t know because at that time there were no martingale probabilities / risk-neutral pricing, they did it differently.

The point here is that as long as you can replicate this claim C(T), and there is a martingale probability this formula is correct for European type payoffs.

Note: This formula doesn’t tell you how to replicate, you’re going to need a different model. Secondly, in practice, you cannot typically replicate claims in complicated derivatives such as options. You simply have to approximate and hope the formula holds.

Lol…theory, emmiright?