Model Independent Option Pricing

Model Independent Option Pricing

The last time I will talk about pricing options void of models.

I originally wrote this as a twitter thread, but I thought it might be useful to send it out on substack as well. The style and flow might be a little different for that reason, it will be dry, but you will hopefully absorb the key information, and I’m sure you can forgive me for the lack of literary flair you have become accustomed too.

Lets jump into model independent pricing of Options, this section is going to be the last time we look at option pricing without the use of mathematical models. Being that this isn’t truly a MS Finance class I am going to skip over a large chunk of this section so we can get to pricing options with models, which is more helpful. However, we have to briefly cover this section, because once again, we are build the foundation for what we are going to cover in future sessions.

Ok, now that the preface is out of the way, lets go, you normally need mathematical models to price options (duh), but what we will be able to achieve here is to get some inequalities (bounce) in the prices of options.

The key goal here is to look at the relationship between American Calls/Puts vs. European Calls/Puts and Price of the Underlying.

To begin lets outline some notations:

European options are lower case.

American options are upper case.

t = Time

C or c = Call

P or p = Put

s = Price of the Underlying

k = Strike price

Relation 1:

The price of a European call at anytime has to be less than or equal to the corresponding American call which has to be less than or equal to the the underlying at anytime (t).

One might ask why this is the case? In American options, the buyer can exercise anytime before maturity which means the buyer has more “options”, more flexibility, therefore the American option holds at least as much value as the European (usually more). However, both need to be less than price of the underlying because the payoff of the call options is:

Max (s(τ)-k,0)

(Where in the American option (Tau) τ= exercise time)

The payoff is always less that s(τ). (Price of underlying at expiry.)

To put it another way, no matter when I exercise this option, I will never get more than the price of the underlying.

Think about it logically, the price of the option cannot be higher than the price of the underling. If it was so, you could sell the option and buy the underlying (arb.)

Therefore the payoff is always less or equal to the underlying.

Relation 2:

Relation number two is the same as above, but the European Put must cost less than the American which must be less than or equal too the strike price, as we established above.

Max(K –S( τ),0) <K

No matter when its exercised the price can not be larger than K.

Relation 3:

This brings us to relation 3, the European version.

This is where things get a bit confusing. The price actually has to be less than the discounted strike price, with European options we can only exercise at time of expiry. So if at maturity the price is less than K, today the price has to also be less or equal to the present value of K.

If we are to assume continuous compounding the formula is simply the right side of the above equation.

This is just discounted K.

To reiterate, we don’t know when the American version is going to be exercised, so price of the option simply has to be less than strike price, but with the European option we know when it will be exercised in the future (at expiration), therefore we can say price is less than discounted strike price.

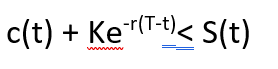

Relation 4:

This brings us to Relation 4.

It says the price of a European call at time (t) has to be larger than the price minus the discounted strike price. (If the underlying pays no dividends.)

To illustrate this, we are going to look at an arbitrage play. But first, lets move the formula around a bit, we are going to move the (-) sign otherwise we can get confused on what we need to buy and sell with the arb strategy.

Alright, lets get into the trade.

Strategy: Sell short one share and if the formula above is true we will have more than enough to buy 1 call, because S(t) is greater than c(t). The last thing we need to do is invest discounted Ke-r(T-t) in the bank and earn a rate of r.

What we will show by doing this is that we will have extra money up front and no loss, sooo…arbitrage. We will also conclude that this cannot hold forever, but the original relation 4 formula must hold.

Ok, if we implement our strategy correctly (sell 1 share short, buy 1 Call, invest K and earn interest) we will only need to check what happens at maturity, because with this strategy there are only payments at T (expiry). So set it and forget it.

At expiration, there are two relevant scenarios, either the Call is going to be in the money or out of the money.

If the underlying price is larger than K at maturity, I exercise the option by buying S(T) (the share) for K. Can I do that? Well I have K stashed away in the bank, remember we initially put K in the bank and it is growing at rate (r) exactly to K.

Here is what it would look like,

Step 1: Exercise the option and pay with K.

Step 2: Receive 1 share of the underlying.

Step 3: Using that share we close our short position.

The result is an already known net gain with no risk. Arbitrage.

Our second scenario is that the option expires and the stock is less than the strike price, so we simply do not exercise the option and buy our short position back with our cash.

In other words, I still have the short position in the underlying, but that’s ok because K (which is what I have in the bank) is more than the spot price.

All we need to do is use our invested cash (+ interest) to buy back our short position which is now less than K.

In either scenario we are ok.

I don’t think I need to explain to anyone why this can not continue. Someone will spot the arb and suck the value out of it immediately. Hence, the European call has to be more expensive than the price of the stock minus the discounted strike price (relation 4).

Next week we are getting into Risk Neutral Pricing. Which is probably, conceptually, the most important part of this series we are doing.