DeFi Yield

DeFi Yield

Quick thought on hunting for yield while waiting for options.

I love trading Bitcoin options, but this has become difficult for me as an American because Deribit (the largest options trading exchange and the one with the most liquidity) banned US customers. Hopefully, in the future this will change, but for now I am forced to find another vehicle that both satisfies the dopamine receptors and pumps out yield. Enter DeFi.

It turns out, as I am sure most of you know, there is a section of the crypto space known as Defi, and in this arena you can provide liquidity via pools. In return, you earn an interest rate. Now these pools are not as straightforward as one would have you believe. To start with, you have to be wary of impermanent loss which is essentially arbitrageurs eating your lunch. You are also exposed to the directional risk of tokens themselves. Nevertheless, it turns out when you enter a pool paired with a stablecoin (wETH/USDT) the pool will act almost like a strip of short puts. If there was such a thing as “pool greeks” you would be short vol and long theta.

Let’s take a look at a quick example, to enter the pool you would deposit 1 ETH and $2500 USDT (pools must be entered in 1:1 ie, 1ETH=$2500), this leaves you exposed to two things besides the arbitrageurs, the failure of USDT (unlikely, but there are ways to hedge) and the directional risk of ETH. To negate directional risk you would short the ETH perp leaving you delta neutral. What you're left with is an overall position that acts like a short strangle.

I’ve already gone far beyond what I intended to talk about today but I just wanted to make the point that DeFi strategies can be used to compensate for the dopamine that Deribit and the US government stole from me. If this is a strategy that I want to deploy, I need to at least have a fundamental understanding of DeFi and a sliver of confidence that it all won’t blow up whenever the next catastrophic market crash occurs, right? This is actually what I wanted to cover, so let’s jump in.

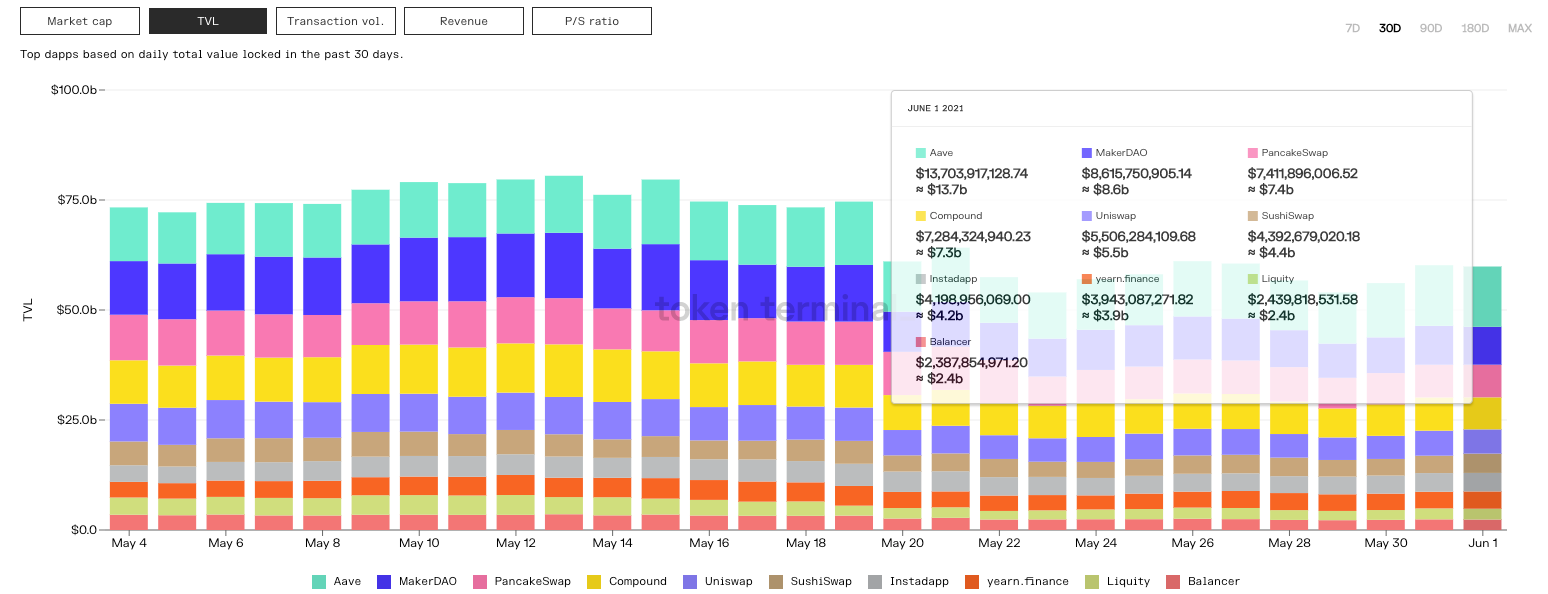

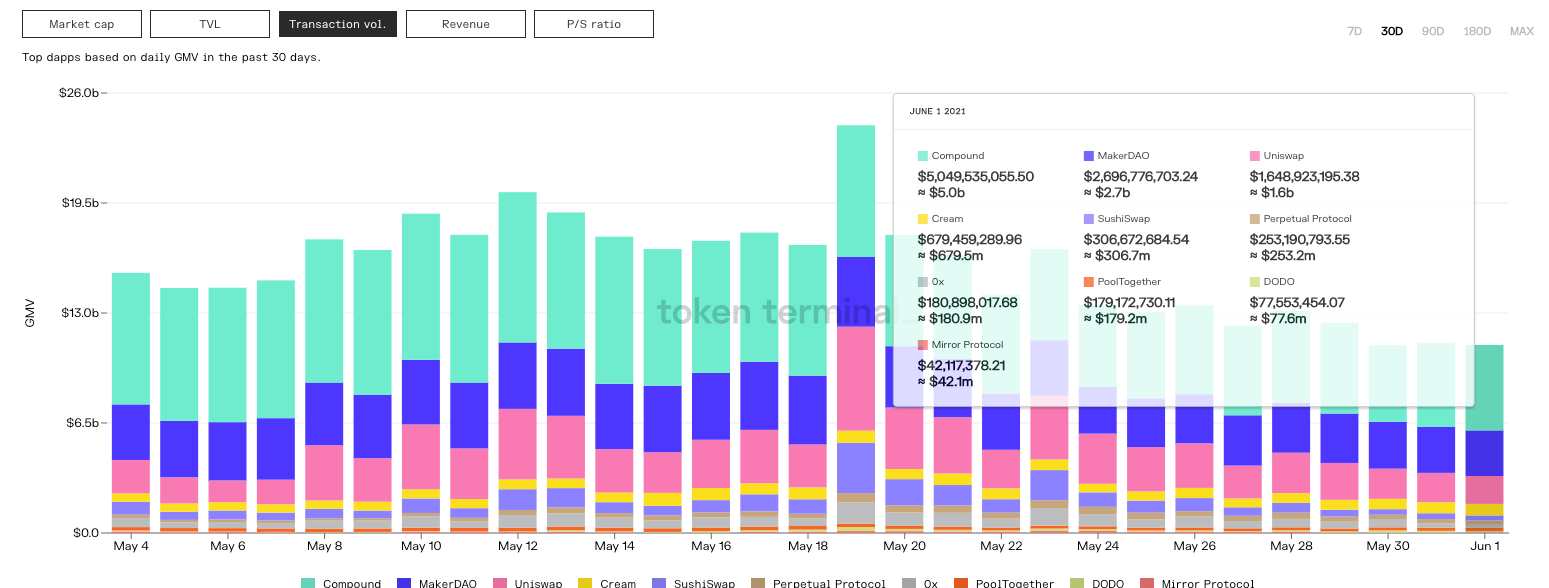

During the most recent selloff, the Defi sector performed mechanically quite well. As CEX’s (Centralized Exchanges) were overwhelmed and failing, DEX’s (Decentralized Exchanges) kept trading almost seamlessly. A common metric we look at to measure health is the Total Value Locked (TVL) in protocols. While TVL (another way to think of AUM) dropped off from its high of just over 75B it’s now back to 61B, which is around the same level we saw just before the crash. Transaction across Defi during the crash experienced a violent spike as people fled to the relative safety of stablecoins, and then proceeded to drawdown as the dust settled, but are now reassuringly back to pre-crash levels. This last crash, in our opinion, highlights the antifragility of the system. *Again, just to clarify, we are simply talking about mechanics not token prices.

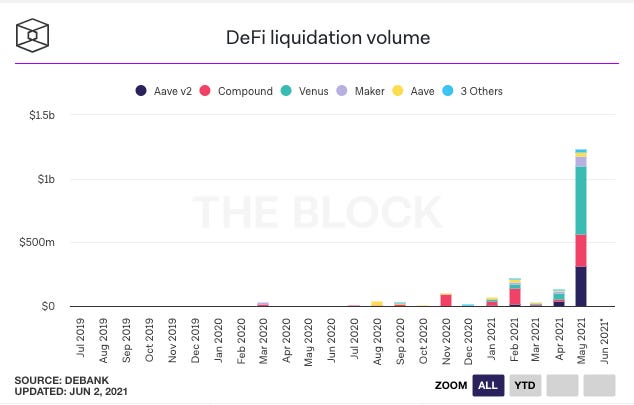

What makes this more impressive is that this was one of the largest Defi liquidation events in history, clocking in at around 1.25B in assets evicerated. Ouch.

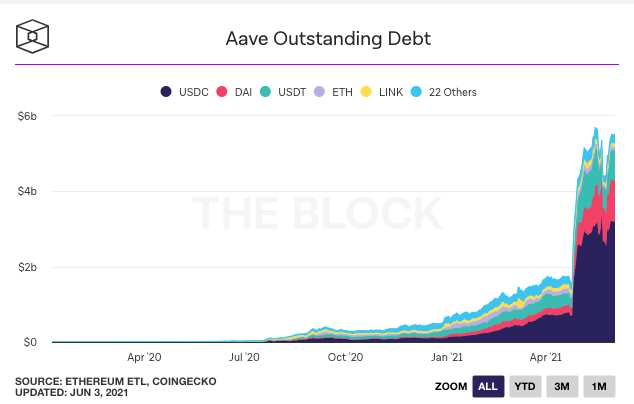

Even after that shock, AAVE’s outstanding debt is back to the level it was before the crash at around 5.5B. This is a good sign, it would seem investors faith in these protocols has grown over the last few years, had this happened 3 or 4 years ago I don’t think things would have fared so well, anyway the ferocity of the rebound also tells me that investors are on the hunt for stable yields in a weak market. Over time as the market matures, this should become the norm and yields will ultimately come down to a “normal” level (whatever that means in crypto.)

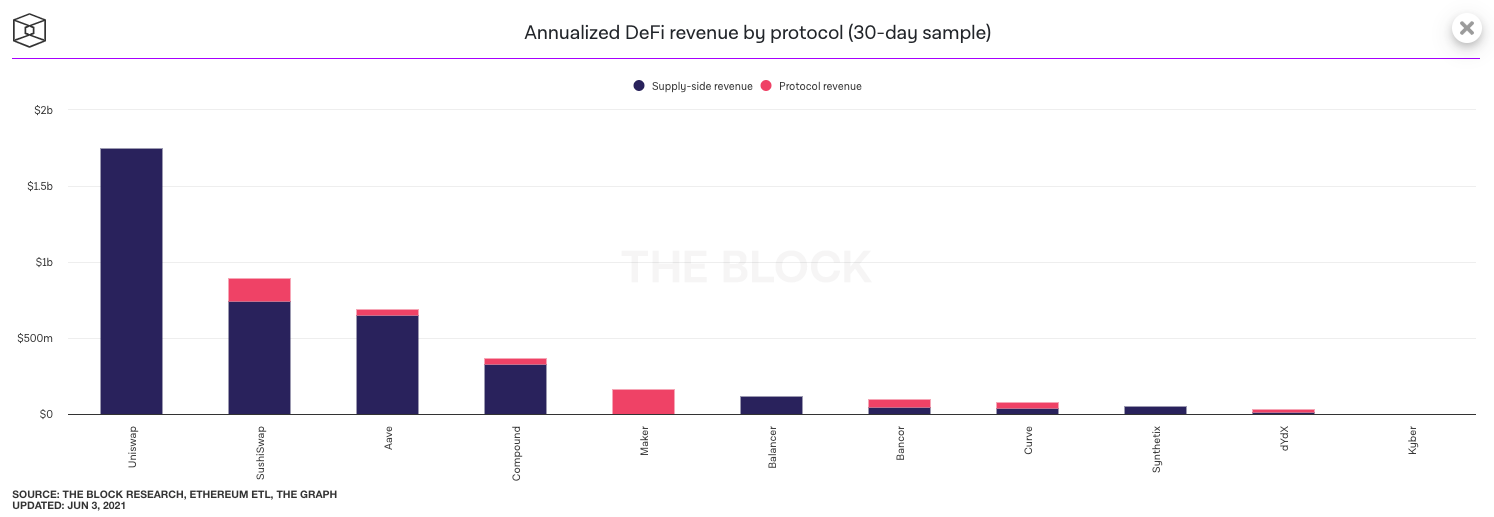

At the moment it looks like AAVE has about 22B dollars locked up on their platform, that’s not an insignificant amount, so who is using these DeFi protocols? Let’s briefly take a look at some stats to try and peer behind the curtain.

According to a new report by PwC and Alternative Investment Management Association (AIMA), Crypto hedge funds now manage about 3.8B in assets, up from 2B the year before.

“Released Monday, the third annual Global Crypto Hedge Fund Report, co-authored by Elwood Asset Management, shows that 31% of crypto hedge funds use decentralized exchanges (DEXs), with Uniswap being the most widely used (16%), followed by 1inch (8%) and SushiSwap (4%).

While bitcoin remains far and away the most popular asset among funds, Ethereum’s native token was included in 67% of investments. Crypto hedge funds are also involved in cryptocurrency staking (42%), lending (33%), and borrowing (24%).”

Ethereum has the first-mover advantage, it’s the biggest ecosystem in the space and has the largest market cap, but it will be interesting to see how Solana holds up and tries to compete moving forward. As Arca pointed out in last month’s report BSC and Solana are becoming the first two real competitors to ETH.

While Bitcoin lacked a positive catalyst, the market turned its attention to the rise in protocols and platforms, including Ethereum, Binance Smart Chain, and Solana, the latter two becoming the first real competitors to Ethereum since the inception of smart contract technology. SOL gained +127%, BNB gained +84% and ETH gained +39% in April.”

-Arca Digital Asset Fund

Ok, so institutional funds are clearly interested, and it’s easy to see why. Not only can you earn interest on some of the tokens you hold by adding them to LP pools, but these protocols also have cashflows, and sometimes they share their revenue with token holders for simply holding the token, almost like a dividend yield. This intuitively makes sense to the tradfi lifer. Furthermore, it seems like the relative strength of the sector as a whole has gotten fairly robust. Even after a monster crash in mid-May, nothing broke, it carried on permissionlessly, as it should.

As I said, this world of farming yield has become my focus ever since I was booted from Derbit because I was born in a certain geographical location. There is however a silver lining, options on-chain are coming and coming quickly. This means permissionless options trading, these protocols are agnostic of geography or politicians, which has its pros and cons, and only time will tell if we succeed in building the future of France. One of the final hurdles is getting the liquidity to follow the innovation, which will take time. Bumps are bound to happen, but they shall be smoothed out as the space emerges from its nascency, and I for one, have high hopes for France.

If you want to learn more check out Dopex, Opyn, or Zeta.

_Variant