Breaking Down ETH as a Bond

Breaking Down ETH as a Bond

A closer look at the article by Arthur Hayes.

Over the last few weeks, we have been working our way through some heady financial equations and concepts, now its time to put some of what we have learned into practice. In a recent article Arthur Hayes (my favorite crypto/finance writer) bridged tradition finance and crypto in his signature style. He postulated that ETH can be valued like a bond with coupons and from there extrapolates the present value of Ethereum. This concept should sound similar if you have been paying attention. All that being said, I want to briefly break down how Arthur valued ETH because I think it could be useful.

For those of you who want the TLDR;

The article argues that you can borrow USDT and buy 32 ETH then stake that ETH in a validator to earn anywhere from 9-11.5%. You can therefore value your 32 ETH as a 5, 10, or 20 year bond.

The goal of Arthurs article was to value ETH like a bond with the hopes of giving normie financial advisors something they could relate too.

But first, to complete this valuation we need a few metrics, spot price of “bond”, coupon, discount rate, years to maturity, and payment frequency. We don’t know the coupon rate for certain because ETH is in fact not an actual bond, so we must make some assumptions. First, Arthur pulls the research below from Justin Drake and assumes that people who stake ETH could see an APR of 9-11.5%. He notes that whether or not those numbers are correct we are using them for the sake of the example, but they do seem reasonable.

Secondly, we need to find the discount rate, for those of you who don’t know, the discount rate is the interest rate you are charged to borrow money. Most of the pools of capital Arthur is speaking of are big enough to borrow money close to the curve, meaning very low rates. The rest of us in the proletariat class must borrow from places like Aave, or Solend, so I will be using their USDC borrowing rates.

Ok, lets break it down, here are the steps straight from the man himself.

1. Borrow USD for a term, and then purchase ETH at the current exchange rate.

2. Stake the 32 ETH, and earn rewards in ETH terms.

3. After a certain number of years, sell the 32 ETH and accumulated rewards for USD.

4. Repay the USD loan.

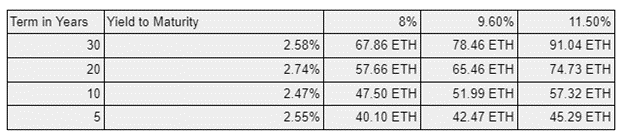

The following table is the ETH bond’s present value in ETH terms.

Remember, we are assuming that 1 bond = 32 ETH. The chart above says that if you were to invest 1 bond (32 ETH) into a validator and earn 9.6% for 10 years, that bonds present value is actually 51.99ETH.

To simplify:

If ETH is 3k: $3,000*32 ETH = $96,000

PV: $3,000*51.99 ETH = $155,970

The PV is higher than the current value so this would be considered a good investment (theoretically.)

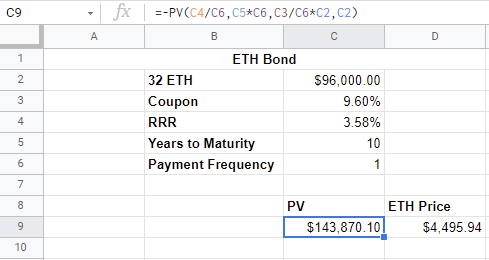

We’ve covered the PV discount rate formula in the last few articles I’ve written so you should understand the math, but the real world (fast) way to calculate this is just use Excel. I’ve screen grabbed my sheet for your convenience.

*This is assuming we aren’t compounding, if we were compounding multiple times a year the numbers would look even more compelling.

=-PV(C6/C8,C7*C8,C5/C8*C4,C4)

To break it down, 32 ETH right now is worth 96k, we are assuming (like Arthur) we can get 9.6% a year on our bond, we can borrow USDT to buy ETH from AAVE at 3.58% (this is variable and will change but for the example sake we are taking a snapshot in time.) We are also assuming we will hold this bond for 10 years at which point we will withdraw our ETH (this isn’t possible at the moment) and pay off our loan, and lastly we are assuming we are being paid our interest one time a year. With these values we can calculate the present value of the bond (143k) which means the PV of 1 ETH is $4,495. Now if we truly believe this valuation, then buying ETH at 3k is obviously a steal and you would be more than willing to pay up.

Like most things in finance this is theoretical, what can go wrong will go wrong. For this to actually come to fruition everyone would need to share the belief that ETH can be valued in this way and then act upon those beliefs. Meaning people need to buy heaps of ETH and stake it until the current price of ETH matches the PV equivalent.

As someone who spent a lot of time in a class listening to someone else drone on about this type of thing, I like looking at this math because it makes sense. In fact, I’ve had conversation with multiple family offices about this type of trade, long story short, the idea of ETH bond resonates. They agree with the thesis and are more than happy for something a tad more stable and a little less degen.

For me personally, if I really believed ETH’s valuation is akin to a 10yr bond paying 9.6%, the play is to just BTD. Why, because if everyone else believes the same thing, it wont take 10 years for the price to meet its theoretical valuation.

Bonus:

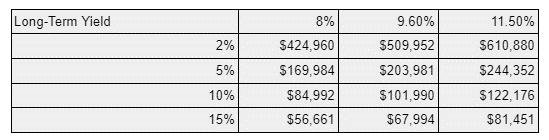

Last thing, in the article Arthur also values ETH as a perpetual bond. Meaning it has no maturity date, which is pretty accurate as there is currently no way to withdraw your ETH from a validator. I’ll let him explain below.

UK nominal long-term yields were basically 5% or lower for most of the few hundred year history of this debt instrument. Therefore, let’s assume that the long-term yields from now going forward are 5%, and that the ETH rewards are at the low end of our forecast at 8%. We arrive at a terminal present value of an ETH cash flow stream of 51.20 ETH. The required input for this ETH cash flow stream is 32 ETH.

If we use this to determine the bond implied value of ETH, we arrive at the below chart. The values are simply the multiplication of [Spot * Present Value of ETH Rewards].

Wild and unreasonable in my opinion, but still fun to look at and dream.