Bond (Finance Course 2.2)

Bond (Finance Course 2.2)

Calculating yields

I originally wrote this as a twitter thread, but I thought it might be useful to send it out on substack as well. The style and flow might be a little different for that reason, but you will get the key points and I’m sure you can forgive me for the lack of literary flair you have become accustomed too.

We are going to cover one more thing on bonds and then get into how you can use the information we have been talking about in the real world. This is going to be a bit more advance, while at the same time being tedious (and kind of boring) but hang in there. We will need this when we start pushing into stochastic behavior later.

Ok, let’s assume there is a 6-month zero coupon bond with a face value of 100 that we can buy right now for $98, in this case we are going to also assume there is no arbitrage in the market.

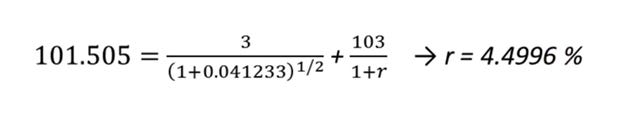

We see that there happens to be a coupon bond that pays $3 in 6 months and $103 in 12 months (so the face value plus a coupon at the end of the year.) That bond is currently priced at $101.505.

The question becomes, is this enough information to conclude what the yield of the 1 year zero coupon bond with a face value of 100 should be? Or in other words, what must the yield be so that no arbitrage exists.

Well here is how we calculate the yield.

What we need to do first is combine the two bonds to create something that pays nothing in 6 months but something in 1 year. So we are essentially going to create a short position with one bond and a long position in the other, this will cancel the coupon in 6mo and we will be left with a payment in 1 year.

When combined, this effectively creates a 1 year 0 coupon bond. We will then apply the law of one price (create same payoff in a different way) to find the price, and if we have the price we can compute the yield, voilà.

So lets go…

First lets replicate a 1 year 0 coupon bond by using a 6 month 0 coupon bond and 1yr bond.

Buy: 1x coupon bond for $101.505. (This is the bond that pays $3 in 6 months and $103 in a year.)

We now need to kill that yield, so we…

Sell: .03 units of the ($98) 6-month bond. (Which means we will pay $3 in 6 months.)

Math:

Cost: 101.505-.03*98 = 98.565

So $98.565 is the cost of setting up this portfolio.

In 6 months, we have to pay $3 for our short bond, and receive $3 as a coupon, cancels out. In 12 months, the 6 month bond is over and we are left with our 1 year bond which pays us $103

So effectively what we did was invest 98.565 to receive $103 in 12 months.

We can now compute the rate.

98.565 = 103/1+r’

r=4.4996%

This is a complicated way to get the rate, but it just shows how you can replicate one kind of payoff (1 year 0 coupon bond) with a portfolio of other assets. And now we know what the payoff is worth, because the value has to be equal to the cost of the replicating portfolio.

Ok, this is the main economic principle we are trying to get across.

If we can replicate something, the cost must be equal to the value of the replication. If its not, arbitrage is possible.

Lets go ahead and beat a dead horse, because why not. Here is the easier way to do the same thing.

First, we compute the yield using this present value formula.

We know the spot rate is $98, and the exponent is ½ because its maturity is in 6 months. (1 year would equal an exponent of 1 if compounded once a year.)

Then we look at the 1 year coupon bond. We can decompose what it pays after 1 month and what it pays after one year. After 6 months it pays 3 dollars, but we can now price 3 dollars because we have the spot rate for 6 months (4.1233%).

We know we receive 103 dollars at the end of our 1 year bond, so all that’s left to do is solve for r.

As you can see we get the same solution we got from the replication argument.

r= 4.4996%

This is just a faster way to do it, but the other way showed you the logic, or in other words the law of one price.

Next lets briefly talk about forward rates.

The idea is that by trading bonds with different maturities today, you can replicate a trade where you invest $1 one year from now and receive a payoff 2 years from now. So invest at a future date and receive a payment at an even later date.

The rate corresponding to the change in the investments value starting in the future and ending at a later date further in the future is called a forward rate…mind blown.

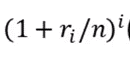

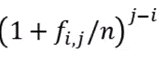

So, here is the formula.

Rk = annualized spot rate for k periods from now

Fi,j = forward rate between the i-th and j-th period from now (j is larger than i)

Lets do a numerical example.

We have a 1 year 0 coupon bond that cost $95

We also have a 2 year 0 coupon bond that cost $85

Compounding is done once a year.

Lets say we want to compute the rate from year 1 in the future to year 2.

We use the formula above

If we use the right hand side of the equation above we can calculate (1+ri)1 which is just (1+r1) which gives us 5.2632%.

Add 1 and you get 1.052632, now multiply that by the forward rate f1,2 rate. (far right of the formula).

The right side has to equal the left-hand side, which is r2/1 and if you calculate that you get line 3 below. So it would seem our forward rate is 6.7416%.

This is the rate you can guarantee yourself today if you invest that dollar 1 year from now.

But like all good obsessive-compulsive mathematicians let’s check that using another example.

Assume face value of the bond is 100 and you believe rate (f1,2) is too high, meaning the price is too low and you want to take advantage of this because you’re a degenerate and you can’t stand to leave a penny on the table…err…I mean, you simply believe the rate will be lower in the future.

The first thing we need to do is buy the cheap bond and sell the expensive bond.

The idea here will be to invest 0 today and have positive profits in the future.

Now, because you believe the price for the two year is too low, you will:

Step 1: Buy +1 2 year bond for a price of $89

Step 2: Sell enough of the 1 year bond to get exactly $89

89/95 units of the 1 year bond = $89

Now we are net 0

What happens next?

After 1 year: We must pay back our short position (89/95*100 = $93.6842)

After 2 Year: We receive $100, from our long bond.

Meaning second year return is 6.74%

In other words, investing ~$93 for one year and getting $100 back will reward you a ~6.7% return. Which means what we calculated above was correct, however if in one calculation we got 6.7% and in the second we got 6.5%, there would be an arbitrage to take advantage of.

Ok, so between Part I and Part II we now deeply understand bond yields. I’m sure your significant other will be incredible impressed; I know mine is. lolz

Up next we break down the work Arthur Hayes did in valuing ETH as a bond.