An Overview of PowerPools by Powertrade.

An Overview of PowerPools by Powertrade.

Hedging LP risk using options all on one platform.

Obsession and AMM’s

Obsession looks vastly different to different people; to some, it looks like exercising 5 hours a day, to others, it looks like collecting the hair of their favorite celebrity to make life-size dolls. For me, it's anything to do with finance, options, earning yield, structured products, and Ponzi games all driven by a thrill-seeking personality type and a minor gambling addiction.

A couple of weeks ago, I came across something which rolled a lot of what I just listed into one product called the Powerpools. These are a beautiful amalgamation of finance, options, and probably a structured product in the finality of their evolution. Over the following couple paragraphs, I will attempt to explain how these pools work, how they are different from UniV3, and how you can earn a very, very low-risk yield by using them. All I ask is that you try to tamp down your degeneracy for the next few minutes and think about earning interest on assets like a professional.

Uniswap AMM (Automated Market Maker)

For brevities sake, I will operate under the assumption that most of you have used LP pools before and have a basic understanding of what they are, but just in case, here is the TLDR.

You provide two tokens (ETH-USDC) to a pool.

Traders trade between those two tokens, and the pool will act as a market maker.

You will then be rewarded with the fees (interest) for providing liquidity.

When liquidity providing (LP) to a pool on UniV2, you simply provide the two tokens (let's say ETH-USDC); the algorithm then spreads that liquidity along the X*Y=K curve.

ETH_quantity(X) * USDC_quantity (Y) = constant_product (K)

This model ensures there will always be a constant number of tokens in the pool, but the model has flaws. For one, this isn't exactly capital efficient. For example, suppose ETH is trading between $2600 and $2900, but only 10% of your money is provided within that range; you are effectively earning a fraction of the fees you could potentially be making. UniV3 addressed this problem, LPs don't just provide assets and allow Uni to spread them evenly; as a liquidity provider, you can choose the range you allocate your cash within.

This ability to concentrate liquidity within a specific price range allows for much higher capital efficiency, which is excellent. However, there are still a few problems that need to be addressed. First, it's worth mentioning the painfully obvious. When interacting with ETH, the astronomical cost users suffer generally makes it infeasible for smaller players and even unattractive for medium-size players to participate. If you wanted to moving liquidity from one range to another its going to take a certain amount of transaction, each of these transactions comes with painfully high gas fees; call me old-fashioned, but simply moving one's liquidity shouldn't cost 5-10% of the position itself.

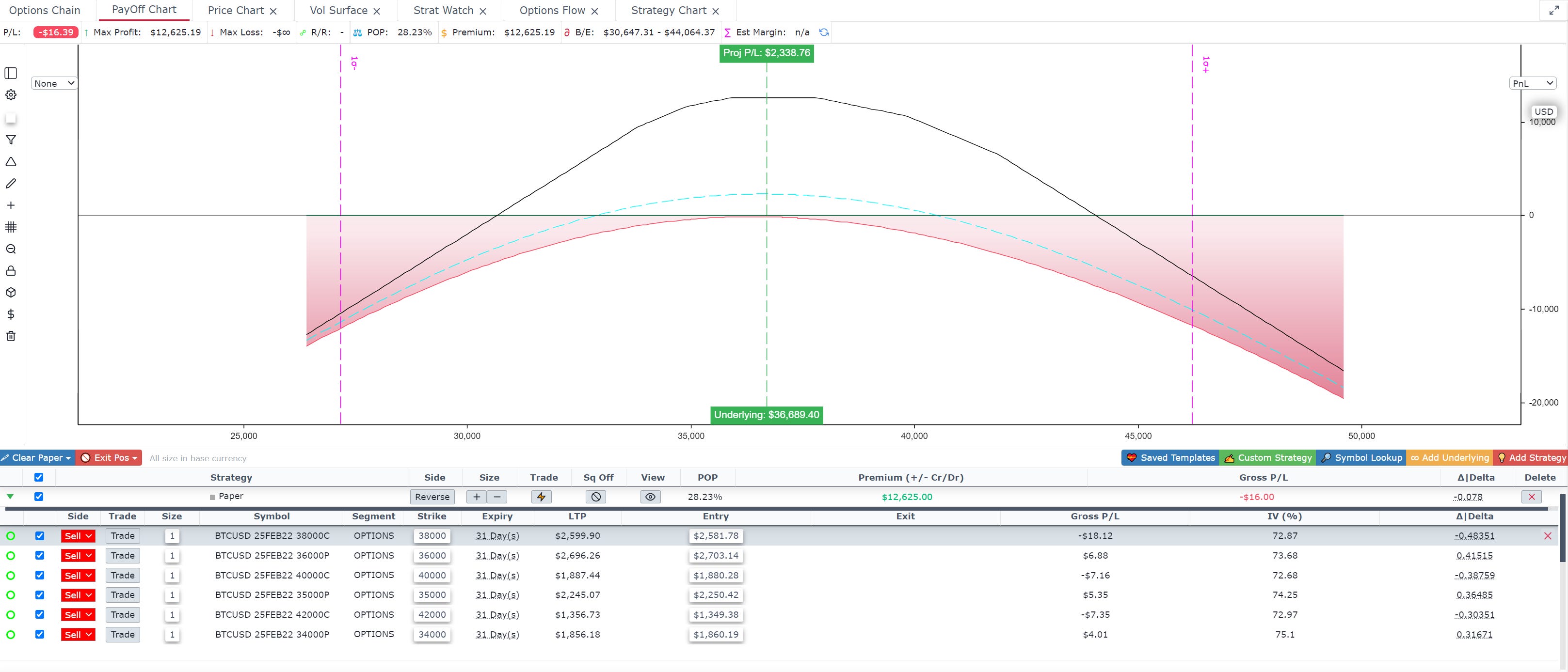

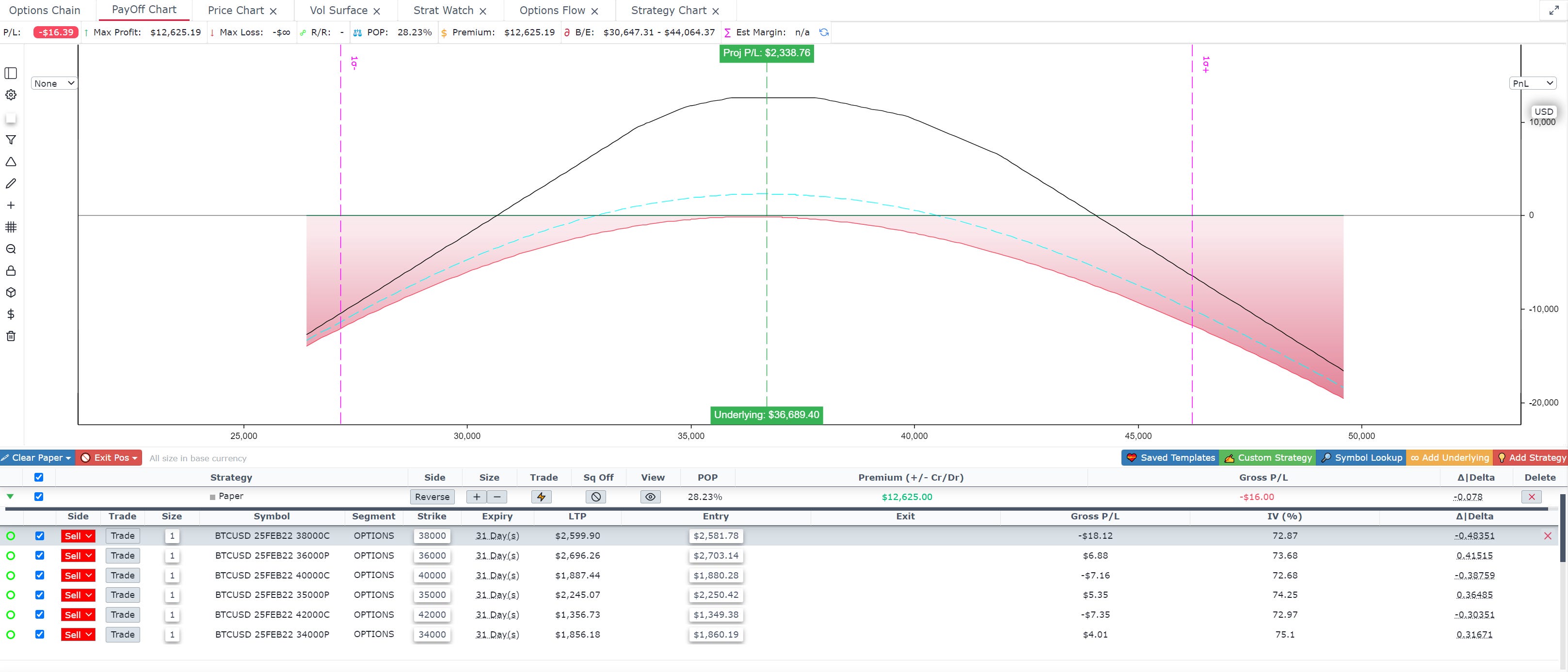

Secondly, and perhaps a bit too complex for our purposes but also worth mentioning, is the idea of volatility and loss. When you enter an LP pool, you have effectively entered into a short gamma position, now this may not always appropriate or desired. You can actually model this reasonably closely with a continuous strip of short strangles. A short strangle works well if the volatility of the underlying remains relatively low and the price of the underlying moves very little. However, any outsized move in the underlying will leave you rekt, thanks for playing. The chart below visualizes this well, and we will go deeper into this concept in future articles. Still, right now, we need to understand that as the underlying moves violently, we will violently lose money (or lose the opportunity to make money.)

Let's recap the three issues I have with entering pools and transacting on the Ethereum chain.

Capital Efficiency

Gas Fees

Short Gamma (Loss)

The Powerpools set out to meet the first requirement of concentrated liquidity while remedying the last two drawbacks of traditional AMM's. The Powerpools are similar to UniV3 in that you can provide your liquidity to any part of the curve. For example, if ETH has been trading within a range for the last week and you believe it stays within that range, then by all means, park your liquidity within that range. What happens next is where the Powerpools differentiate themselves. The liquidity provided is laid out in a strip of pre-computed buy and sell orders on Powertrades CLOB (Central Limit Order Book). Furthermore, the fees are then accrued in the term (Y) currency (USD). This allows for a more straightforward computation of yield and management of positions being that you don't have to factor in the implied delta of holding X currency beyond the fee event.

Anecdotally, I can tell you transacting on ETH is not only an abysmal user experience in its current state (looking at you metamask), but as we have discussed, it's also incredibly expensive for the average user. I have personally experienced sending a test transaction of $100 only to pay $30 in gas. So what happens if ETH makes a move and starts trading outside your defined range? This is the benefit of the hybrid AMM/CEX model; you can now pull your liquidity from the pool and enter it within a newly defined range of your choosing whilst paying 0 fees. You heard that right, 0 fees.

Here is a clarification from Richard Hodges (Powertrade Head of Risk) posted in telegram a few days ago.

In one of Powertrades more recent blogs they outlined a few more benefits of using the PowerPools. For your convivence I have copy pasta’d them below.

Flexibility – Rather than working on an RFQ model, our AMM pools spread liquidity across the entire range as limit orders, taking advantage of the fine resolution of the exchange's flexibility.

No Maker Fees – Because Power Trade charges no maker fee for PowerPools, the trades executed against them are frictionless, meaning that our clients pick up 100% of the mark-up (fee) they specified when creating the pool.

No Network Fees – Because there is no smart contract involved, there are no network fees. This means our clients can create, modify, fund, defund and destroy pools at will with no costs. This allows them to re-adjust pools dynamically to maximize returns without worrying about paying more in gas fees than they are making – this is of particular benefit to "the hoard" of smaller participants who are currently priced out of the Uniswap market.

More Efficient – PowerPools turn out to be more efficient than smart contract- based pools, because they are continually trading. In our tests we have observed between 15% and 100% higher yield. We believe that this is because PowerPools are continuously, relentlessly trading. They don't wait for someone to want to exchange a block of money. They hold the trade out on the order book. If a client doesn't take it, an arbitrageur will.

Short Gamma

We have established that the Powerpools allow for concentrated liquidity ie. capital efficiency, and they have solved for the high fees levied on users by some L1's and their Dapps. Finally, we need to tackle the short gamma problem or what traders call Impermeant loss, and what sane people simply call, loss. This is the most interesting feature in my opinion.

To re-iterate what I said above, when you provide liquidity to a pool you are essentially in a short Gamma position collecting Theta. The position can be closely modeled by using a string of short strangles.

Re-posted chart from above.

You don't need to understand Options to understand that while providing liquidity to a pool your PnL will increase while volatility is low, but the PnL of your position gets destroyed every time volatility rears its head, assuming you aren't hedged. The easiest way to say this goes something like this,

ETH goes up in price = Pool sells ETH into USDT on the way up, and you miss out on the appreciation of ETH.

ETH price goes down = pool sells USDT into ETH and you are left holding a bag of ETH which is now worthless in dollar terms.

So the question becomes how do you hedge? Since the Powerpools are built on Powertrade (an Option exchange), its relatively easy. As you earn fees you can decide what to do with them, and you have a few options.

Reinvest fees.

Collect Fees.

Buy fractional option strangles to hedge loss.

Buy factional option straddles to benefit from volatility.

Any combination.

If you really wanted to hedge your gamma exposure, here is an example of a path you could take. Lets say you earned $100 of interest in the first week of providing liquidity. You could choose to reinvest $75 and use the remaining $25 to buy fractions of 3 month strangles. After buying fractionalized strangles for a couple of weeks, you should be fully covered. You will no longer need to worry about the market tanking, or going to the moon. Lets say Volatility starts increasing rapidly, you are short Vega, so your pool will start to lose value in dollar terms, but the strangles you bought (long Vega) will gain value and offset your loss leaving you with a positive PnL from the fees (Theta) you have been collecting.

An in-depth look into the mechanics of why this works and how to manage a position is beyond the scope of this article. Just know there are multiple combinations to choose from when deciding what to do with the interest you are earning, and eventually this will all be automated on Powertrade. In the future, the ability to act as a market maker and be truly neutral will be as easy as clicking a few buttons.

Here is a thread explaining exactly how to use the Powerpools right now.

Backtest

This is all well and good, but do the pools work? Do they deliver on their promise? According to the Powertrade blog they have been running test for the last 60 days and the results have been encouraging.

"These tests have been run in an empty market, where the only counter-party has been a simple arbitrage robot. The robot only traded when it saw a 15bp arbitrage against our pool price and the wider market. The graph above shows the fee returns from the (wide) AMM pools under these non-ideal conditions. In fact, the arbitrage robot made as much money as the AMM, after paying exchange fees on both ends of the trade."

Even in an inefficient market, the Powerpools are still returning over 40%. The team assures me that the pools would be returning over 80% if this were an efficient market. Remember, this result is without reinvesting or buying options to hedge.

But theory and backtests only hold so much weight, so here is a real-world example from a live user.

End

This is a perfect solution for someone like me who is always looking for consistent yield for clients. We aren't looking for degen pools that have the potential to make 1000% but also have equal potential of getting rugged. In fact, making a safe 15% is more than enough and vastly outperforms returns coming from tradfi atm.

Secondly, its incredibly convenient to provide liquidity on a platform that specializes in Options. For now, you do have to hedge manually, but soon, with the click of a button, the pools will buy options on your behalf to hedge out your risk. Also, as much as I love DeFi, I find it somewhat comforting that I can email or message Powertrade if something disastrous happens to my funds. As we all know, when transacting on-chain, a safety net is non-existent, which is a little disconcerting to for large books looking to deploy half a yard.

The Powerpools are the perfect marriage between Defi's AMM's and a CEX's. The evolution of what they are to become over the next couple of years is fascinating. I will keep you up to date on new features as they roll out and returns as I continue to test them for myself.